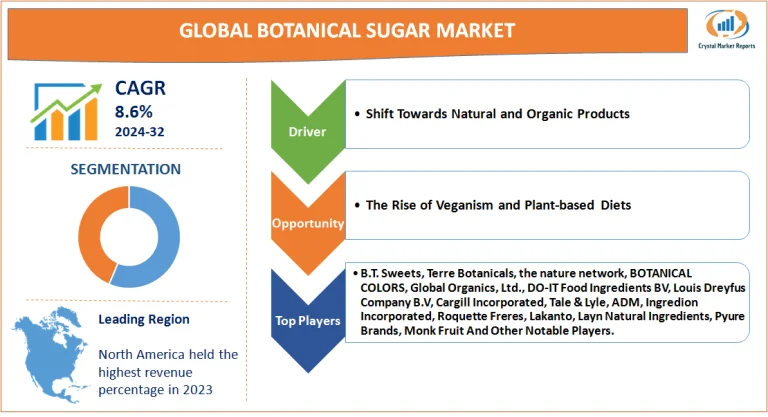

Market Overview

The botanical sugar market refers to the segment within the larger sweetener industry that focuses on sugars derived from plant sources other than traditional cane or beet sugar. This encompasses sugars sourced from coconut palm, dates, agave, and others. A primary catalyst behind the growing appeal of botanical sugars is their perceived natural and wholesome image. Often, they are less processed than their conventional counterparts, leading to a caramel-colored, coarser sugar that retains trace minerals. The botanical sugar market is estimated to grow at a CAGR of 8.6% from 2024 to 2032.

Botanical Sugar Market Dynamics

Driver: Shift Towards Natural and Organic Products

One of the most significant drivers propelling the botanical sugar market forward is the global shift in consumer preferences towards natural and organic products. Over the past decade, there's been a growing distaste for synthetic and overly processed foods, with many consumers now associating them with various health concerns. Botanical sugars, being derived from natural plant sources, fit perfectly into this new paradigm. A notable indication of this trend is the global surge in organic food sales. For instance, the U.S. organic food market grew by 5.9% in 2019, significantly outpacing the general food market's growth of 2.3%. Within this, the organic sweeteners segment, which includes botanical sugars, experienced an even steeper growth trajectory.

Opportunity: The Rise of Veganism and Plant-based Diets

A prominent opportunity lies in the escalating popularity of veganism and plant-based diets. As more people steer clear of animal-derived products, there's an increased demand for plant-based alternatives in every food category, including sugars.This vegan trend isn't merely anecdotal; studies have showcased its rise. The Vegan Society's research indicated that the number of vegans in Great Britain quadrupled between 2014 and 2019. In tandem, the demand for botanical sugars, which align with vegan dietary principles, has also surged.

Restraint: High Pricing Compared to Conventional Sugars

A primary limitation is the cost. Botanical sugars, owing to their natural and often organic label, come at a steeper price compared to conventional sugars. This price disparity can dissuade a segment of consumers, especially in price-sensitive markets. A direct observation of retail prices reveals this disparity. For instance, while conventional white sugar may retail for $2 per pound, botanical alternatives like coconut sugar often have price tags upwards of $4 per pound.

Challenge: Production Scalability and Consistency

A looming challenge for the botanical sugar market is scalability and consistency in production. Unlike conventional sugar sources like cane or beet which have undergone decades, if not centuries, of cultivation optimization, many botanical sugar sources are still in their nascent stages of commercial production. This can lead to supply chain disruptions, inconsistent product quality, and variability in taste or texture. As an example, agave nectar faced supply chain disruptions in 2017 due to a sudden surge in demand coupled with its long cultivation period. Such challenges underscore the need for better planning and investment in the botanical sugar sector.

Product Insights

In terms of product segmentation, the botanical sugar market has seen several product types gaining significant traction. In 2023, cane sugar maintained its traditional dominance, contributing to the largest revenue share. Its long-standing use in various cuisines and commercial applications ensured its continued supremacy. However, when examining CAGR, coconut sugar experienced the most impressive growth, attributed to its low glycemic index and increasing popularity in health-conscious circles. Following closely were stevia sugar and monk fruit, both known for their zero-calorie sweetness and aptness for diabetics. Date sugar and maple sugar also maintained steady growth, their natural origins and unique taste profiles favoring their adoption. Palm sugar, particularly popular in Asian cuisines, saw consistent demand, while honey, being a natural sweetener, continued its steady sales. Agave sugar, despite its initial boom, faced certain criticisms related to its high fructose content. Monk fruit emerged as a notable entrant, its sweetness derived without the typical calorie count, making it a favorite among health enthusiasts. Yacon syrup, although niche, started making its presence felt, particularly among vegan consumers.

Application Insights

Regarding application segmentation, the food and beverage industry in 2023 was undeniably the primary consumer of botanical sugars, given the universal use of sweeteners in culinary practices. Within this industry, there was a visible shift towards healthier alternatives, with food producers keen on touting the 'natural' and 'organic' labels to cater to informed consumers. The pharmaceutical industry, especially in herbal and natural product formulations, also incorporated botanical sugars, valuing their organic and less processed profiles. Stevia, in particular, was a preferred choice due to its zero-calorie nature. The personal care and cosmetics industry, always on the lookout for natural and organic ingredients, incorporated botanical sugars in various formulations, from skin scrubs to lip balms, promoting the moisturizing and gentle exfoliating properties of sugars. Other applications included their use in industrial processes, although this segment didn't contribute as significantly as the others.

Regional Insights

On the geographic front, North America, in 2023, remained a dominant player, with its vast consumer base and heightened awareness of natural products. The region's affinity for organic and non-GMO products facilitated the robust sales of botanical sugars. However, in terms of CAGR from 2024 to 2032, the Asia-Pacific region is expected to showcase remarkable growth. This can be attributed to the traditional use of products like palm sugar and coconut sugar in local cuisines, coupled with rising disposable incomes and increasing health consciousness. Europe, with its stringent regulations on food additives and a consumer base that highly values organic products, also remained a substantial market, particularly for products like stevia and date sugar.

Competitive Landscape

The competitive landscape of the botanical sugar market in 2023 was characterized by a blend of traditional players and emerging companies focusing on niche products. Key players like B.T. Sweets, Terre Botanicals, the nature network, BOTANICAL COLORS, Global Organics, Ltd., DO-IT Food Ingredients BV, Louis Dreyfus Company B.V, Cargill Incorporated, Tale & Lyle, ADM, Ingredion Incorporated, Roquette Freres, Lakanto, Layn Natural Ingredients, Pyure Brands, and Monk Fruit Corpactively pursued strategies like sustainable sourcing, organic certifications, and innovative marketing campaigns centered around the health benefits of their products. A trend of partnerships between botanical sugar producers and food and beverage companies was noted, aimed at jointly developing new products. Companies were also investing in R&D, aiming to enhance the taste profile of their products and reduce any associated aftertastes, a common concern with products like stevia. The market saw heightened M&A activity, with companies aiming to diversify their product portfolios and enter emerging segments like monk fruit sweeteners. As we move towards 2032, competition is expected to intensify, with market players looking to strengthen their supply chains, enhance production capacities, and engage in strategic collaborations.

Working with the worlds leading market research companies.

Research reports across 90 industries.

Simple license based pricing by individual report.

Trusted by thousands for accurate and transparent reports.

Unless otherwise specified all reports are sent electronically in either .PDF or .DOC file format.

Single User License: It provides product access only to the consumer of the ordered product.

Multi User License: It allows maximum up to 10 peoples within your company to share the ordered product.

Global License: It permits the product to be shared by all employees of your firm irrespective of their geographical areas.

Fore more information on report format options and licensing please visit our FAQ's page.

“Have used several times on various projects. Their team have the ability to source reports that we simply cannot access via other providers. Always quality, accurate reports providing valuable insights into the commodity markets and out team will continue to use.”

“CMR’s level of support was excellent. We provided them with a detailed requirement and they delivered a quality report within the same day. I would not hesitate to recommend them.”

“Rebecca, your report has provided our team with the insights needed to make crucial strategic decisions. From understanding our requirement, making recommendations and then providing samples. You worked with us throughout the project and we couldn’t be happier with the result, will definitely use again!”

sales@crystalmarketreport.com